Hybrid Train Market Overview

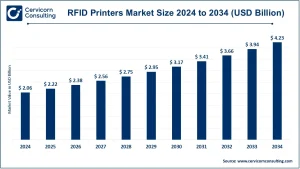

The hybrid train market is witnessing rapid expansion as rail operators and governments worldwide increasingly seek energy-efficient and low-emission transportation alternatives for non-electrified routes. The market was valued at USD 21.89 billion in 2024 and is anticipated to grow to approximately USD 51.36 billion by 2034, registering a CAGR of 8.90% during 2025–2034.

In 2024, Europe dominated global revenue with around 52.7% market share, followed by Asia-Pacific at 21.4%. By propulsion type, the electro-diesel segment led with approximately 38.2% share, while passenger trains accounted for about 58% of total revenues. Additionally, lower-speed trains (under 100 km/h) contributed nearly 46% of market value—highlighting the suitability of hybrid technologies for regional and commuter applications.

Key Market Trends

1. Sustainability-Driven Adoption (Green Fleets)

Rising global emphasis on decarbonization and emission reduction has accelerated the adoption of hybrid rolling stock. These trains, capable of switching between battery/electric and diesel or hydrogen modes, are gaining traction as they lower emissions on non-electrified lines while enabling all-electric operations in urban zones. The European Green Deal and similar initiatives worldwide serve as significant regulatory catalysts for hybrid train deployment.

2. Battery and Energy-Storage Innovations

Technological advances in lithium-ion and solid-state batteries are boosting efficiency and extending electric-only range. As reported by Cervicorn, hybrid train systems have achieved 15–20% improvements in battery efficiency over the past five years, enabling longer service intervals and reduced environmental impact. These innovations, including regenerative braking and advanced storage management, are making hybrid trains increasingly viable replacements for conventional diesel fleets.

3. Diversified Propulsion Architectures

The market now supports multiple propulsion models—electro-diesel, battery-electric, hydrogen-fuel-cell, and even solar-assisted concepts. While electro-diesel continues to dominate (~38.2% market share in 2024), several pilot programs in Germany, Japan, and the UK are testing hydrogen and hybrid-electric variants, indicating a move toward multi-technology integration across regions.

4. Smart Connectivity and Predictive Maintenance

Digitalization is transforming hybrid train operations through real-time analytics, energy management, and predictive maintenance. These technologies optimize propulsion mode selection, extend component lifecycles, and enhance overall cost efficiency. Cervicorn Consulting identifies smart connectivity as a cornerstone trend improving fleet reliability and lowering total cost of ownership.

5. Public–Private Partnerships and Innovative Financing

To overcome high upfront costs, governments and private investors are increasingly collaborating through PPP models, grants, and subsidies. These initiatives help accelerate pilot projects, build supporting infrastructure (charging or hydrogen refueling), and mitigate financial risk for OEMs and operators. Cervicorn highlights such collaborative frameworks as essential for scaling hybrid train adoption.

Market Drivers

1. Policy Support and Decarbonization Mandates

Stringent government emission targets and incentive programs—such as Europe’s Green Deal—are primary catalysts for hybrid train demand. Subsidies, tax incentives, and grants significantly lower capital costs, aligning with Cervicorn’s projected 8.90% CAGR through 2034.

2. Operational Efficiency and Cost Savings

Hybrid trains deliver up to 40% fuel savings and 30% lower carbon emissions compared to diesel-only systems, as per Cervicorn’s analysis. These operational advantages directly enhance lifecycle economics, accelerating fleet modernization for both passenger and freight operators.

3. Technological Progress in Battery and Hydrogen Systems

Continuous innovations in energy storage, fuel cells, and power electronics have expanded hybrid train performance. With 15–20% battery efficiency gains in recent years, hybrid technologies now bridge the gap between traditional and fully electrified systems—offering sustainable, cost-effective alternatives for mid-range networks.

4. Expanding Fleet Deployments and Proven Use Cases

Over 500 hybrid trains were operational globally as of 2023, reflecting the technology’s maturity and reliability. These real-world deployments reduce procurement risk and demonstrate tangible cost and emissions benefits—encouraging broader adoption across markets.

5. Regional Investment and Policy Alignment

Europe’s dominance (52.7% market revenue in 2024) and Asia-Pacific’s rapid expansion (21.4%) highlight strong governmental support and funding. These concentrated markets provide economies of scale for OEMs and component suppliers, fostering cost reductions and accelerated product innovation.

Impact of Trends and Drivers

-

Propulsion Evolution: While electro-diesel remains the mainstream choice for partially electrified routes, advancements in battery and hydrogen technologies are driving diversification toward purpose-built hybrid configurations—ranging from short-distance commuter models to long-haul regional trains.

-

Regional Dynamics: Europe’s policy-driven dominance ensures OEMs continue prioritizing EU-compliant solutions, while Asia-Pacific’s infrastructure investments are catalyzing local manufacturing and technology transfers. North America’s adoption trajectory remains gradual but promising, supported by new federal sustainability initiatives.

-

Application Focus: Passenger transport (58% of 2024 revenues) continues to be the largest application area, leveraging regenerative braking and frequent-stop efficiency. Freight hybrid locomotives are emerging as a secondary growth avenue, driven by energy cost savings and decarbonization goals.

-

Service Model Shift: Smart monitoring and connected maintenance systems are reshaping aftersales and support models, encouraging OEMs to transition from one-time sales to long-term service contracts and digital lifecycle solutions.

Challenges and Opportunities

Challenges:

-

Substantial infrastructure investment needed for charging and refueling networks.

-

Higher upfront capital costs and complex maintenance requirements.

-

Environmental factors (temperature, humidity) impacting battery and fuel-cell performance.

Opportunities:

-

Retrofit market potential: Converting existing diesel fleets to hybrid configurations offers immediate decarbonization gains.

-

Software and analytics monetization: Growth in predictive maintenance, energy management, and “power-as-a-service” business models.

-

Customized propulsion strategies: Multiple hybrid architectures enable OEMs to tailor solutions by geography and operational profile.

Future Outlook

The global hybrid train market will expand from USD 21.89 billion in 2024 to nearly USD 51.36 billion by 2034, growing at a CAGR of 8.90%. Europe will retain its leadership position, while Asia-Pacific emerges as the fastest-growing region due to sustained infrastructure investments and green transport policies.

Technological advances in battery energy density, hydrogen storage, and digital fleet optimization will further reduce operational costs and accelerate adoption. Together with supportive financing mechanisms and sustainability mandates, these developments are set to redefine the future of hybrid rail mobility—positioning it as a cornerstone of global transportation decarbonization efforts.

For a detailed regional and competitive analysis, visit Cervicorn Consulting.