Market Overview

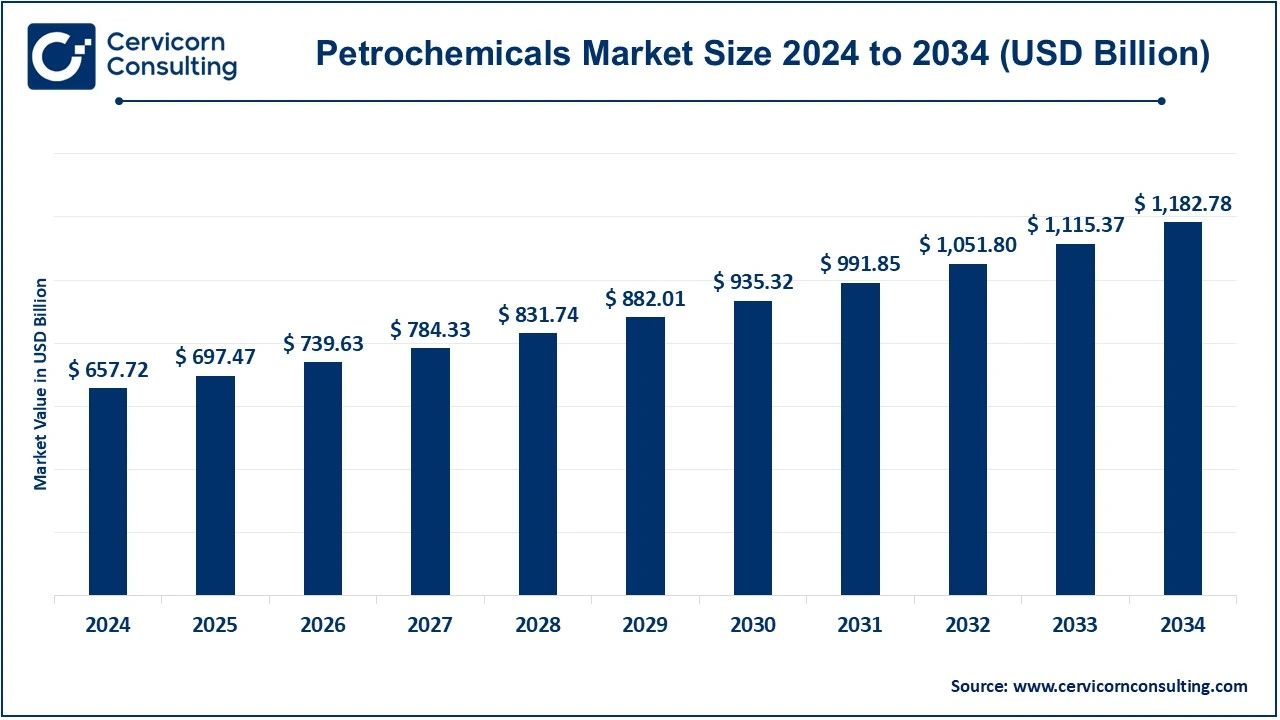

The global petrochemicals market serves as a cornerstone of industrial and economic progress, supplying essential materials that underpin modern manufacturing and innovation. Valued at USD 657.72 billion in 2024, the market is expected to reach nearly USD 1,182.78 billion by 2034, registering a CAGR of 6.04% from 2025 to 2034. Petrochemicals—primarily derived from petroleum and natural gas—form the chemical backbone for industries such as automotive, construction, packaging, textiles, and healthcare. Core products, including ethylene, propylene, benzene, toluene, and xylene, are vital in producing plastics, resins, fertilizers, detergents, and synthetic fibers that fuel global industrial development and consumer applications.

Key Market Trends

1. Shift Toward Circular Economy and Chemical Recycling

Sustainability is reshaping the global petrochemical industry, prompting leading companies to embrace chemical recycling and waste-to-feedstock technologies. Enterprises like BASF SE and SABIC are pioneering circular economy projects that transform plastic waste into reusable feedstocks, significantly cutting reliance on virgin fossil fuels. These efforts align with global initiatives targeting carbon neutrality and improved resource efficiency, reflecting a long-term commitment to greener production models.

2. Growth of Bio-Based and Low-Carbon Feedstocks

A notable market shift is emerging toward bio-based petrochemicals, supported by renewable resource availability and government incentives for sustainable production. Major players such as INEOS and Shell are exploring bioethanol, hydrogen, and waste-derived fuels as feedstock alternatives. This evolution diversifies raw material sourcing, mitigates carbon emissions, and strengthens supply chain resilience amid oil market volatility.

3. Digitalization and Smart Manufacturing Advancements

Digital transformation continues to redefine operational performance in the petrochemical sector. Technologies like artificial intelligence (AI), the Internet of Things (IoT), and predictive analytics are being implemented to enhance process efficiency, predictive maintenance, and energy optimization. Companies including BASF and Dow Chemical Company are adopting digital twins and automation to streamline production, reduce emissions, and improve plant safety, paving the way for Industry 4.0 adoption in petrochemical manufacturing.

4. Expanding Industrial Base in Asia-Pacific

The Asia-Pacific region remains a growth powerhouse, driven by rapid urbanization, industrialization, and expanding consumer demand. Countries such as China, India, and South Korea are investing heavily in large-scale petrochemical complexes and integrated refining systems. This regional expansion not only strengthens supply chain integration but also positions Asia-Pacific as a global production and export hub.

5. Regulatory Support for Sustainable Production

Government frameworks such as the EU Green Deal, U.S. Inflation Reduction Act, and Saudi Vision 2030 are steering the industry toward low-emission manufacturing. These initiatives promote carbon capture, utilization, and storage (CCUS) and encourage investment in eco-friendly chemical production. The regulatory landscape is thus propelling innovation and accelerating the adoption of clean energy-based petrochemical processes.

👉 Get a Free Sample: https://www.cervicornconsulting.com/sample/2544

Market Drivers

1. Rising Demand for Plastics and Polymers

The growing need for lightweight, high-performance, and affordable materials across sectors such as automotive, electronics, and packaging is driving petrochemical consumption. With global plastic production surpassing 400 million tons annually, petrochemicals remain central to manufacturing polymer-based products that enhance durability and energy efficiency.

2. Accelerating Urbanization and Industrialization

Developing economies are major growth catalysts, supported by urban infrastructure expansion and increasing consumer goods demand. The Asia-Pacific region accounts for over 50% of global petrochemical consumption, propelled by industrial clusters in China and India that are fostering downstream production and exports.

3. Technological Innovations in Production

Continuous advancements in steam cracking, catalytic processing, and feedstock flexibility are improving production efficiency while minimizing environmental impact. The rise of modular and adaptive petrochemical plants allows producers to respond rapidly to demand fluctuations and optimize capital investments.

4. Expansion of End-Use Industries

Petrochemicals serve as foundational inputs across industries such as pharmaceuticals, fertilizers, textiles, and automotive manufacturing. The growing reliance on medical-grade polymers in healthcare and nitrogen-based fertilizers in agriculture highlights their diverse industrial relevance and expanding application spectrum.

5. Government Focus on Recycling and Green Chemistry

Governments worldwide are promoting green chemistry frameworks and extended producer responsibility (EPR) programs to reduce waste and encourage sustainable production. This policy environment supports investment in bio-based products and chemical recycling technologies, driving long-term market sustainability.

Impact of Trends and Drivers

The convergence of technological innovation, policy-driven sustainability, and regional industrial expansion is reshaping global petrochemical dynamics. Asia-Pacific is emerging as the manufacturing nucleus due to large-scale investments and domestic consumption growth. Europe is leading in sustainability practices through circular production models, while North America continues to benefit from cost-effective shale gas feedstocks supporting high-capacity ethylene and propylene output.

These transformations are prompting companies to enhance supply chain transparency, integrate life-cycle management, and adapt pricing strategies to reflect sustainability commitments and regional regulatory differences.

Challenges and Opportunities

Challenges:

-

Fluctuating crude oil and natural gas prices.

-

Increasing regulatory compliance costs due to strict emission norms.

-

Geopolitical uncertainties disrupting global logistics and trade.

Opportunities:

-

Rising adoption of bio-based and recycled petrochemicals.

-

Strong investments in carbon capture and utilization (CCUS) and chemical recycling technologies.

-

Expanding market potential in Africa and Latin America through infrastructure and industrial development.

Future Outlook

The petrochemicals market is positioned for sustained growth, with revenues forecasted to reach USD 1,182.78 billion by 2034, advancing at a CAGR of 6.04%. Over the coming decade, circular economy integration, renewable feedstock adoption, and digitalization will define the industry’s evolution. Companies that prioritize sustainability, low-carbon innovation, and regional diversification will capture the greatest opportunities in this rapidly transforming landscape.

As industries worldwide continue to emphasize efficiency, innovation, and environmental responsibility, the petrochemical sector will remain a key enabler of industrial progress—driving economic development and accelerating the transition toward a sustainable global economy.

👉 To Get a Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us