Market Overview

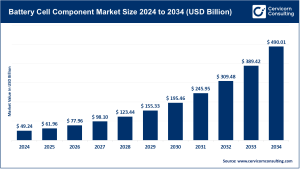

The solar tracker market refers to the segment of solar energy systems designed to automatically adjust the positioning of photovoltaic (PV) panels throughout the day, following the sun’s trajectory to optimize energy capture. According to Cervicorn Consulting, the market size was valued at USD 10.67 billion in 2024 and is anticipated to reach USD 42.43 billion by 2034, expanding at a robust CAGR of 25.07% between 2025 and 2034.

This rapid acceleration highlights the transition of solar trackers from specialized applications to a critical component of mainstream, ground-mounted utility-scale projects. Their adoption is being driven by the growing emphasis on maximizing solar yield, optimizing land use, and meeting global renewable energy targets.

👉 Get a Free Sample: https://www.cervicornconsulting.com/sample/2557

Key Market Trends

The solar tracker industry is witnessing notable transformation influenced by advancements in technology, evolving energy policies, and rising renewable adoption across regions. Key trends shaping the market include:

1. Technological Advancements: Emergence of Smart and IoT-Enabled Trackers

Modern solar trackers now incorporate IoT connectivity, AI-driven analytics, and remote control systems that enhance precision and operational efficiency. These systems dynamically adjust panel tilt based on real-time environmental data—such as solar irradiation and wind conditions—resulting in improved performance and reduced maintenance costs. Smart trackers with predictive algorithms are increasingly being deployed across large-scale solar farms to maximize uptime and energy yield.

2. Rise in Dual-Axis and High-Precision Tracking Solutions

While single-axis trackers continue to dominate the market for their cost-effectiveness, the dual-axis segment is gaining ground, particularly in regions with high solar irradiance or constrained land availability. These systems ensure optimal alignment throughout the year, significantly increasing energy generation per unit area. Cervicorn Consulting reports growing interest in dual-axis trackers for premium projects and high-value sites, especially in regions with strong sun exposure and limited land area.

3. Supportive Renewable Energy Policies and Incentives

Government initiatives such as feed-in tariffs, renewable portfolio standards (RPS), and investment tax credits (ITC) are key enablers of tracker adoption. Policies aimed at expanding solar generation capacity are encouraging developers to integrate tracker systems that offer higher energy output. This alignment between regulatory support and performance-oriented technologies is accelerating global tracker installations.

4. Land Use Optimization and Balance-of-System (BOS) Integration

The decreasing cost of PV modules has shifted developers’ focus toward improving system-level economics. Trackers play a vital role by increasing yield per hectare, enabling better land utilization and cost savings in balance-of-system components. Manufacturers are collaborating with EPC providers to offer streamlined installation processes, modular designs, and reduced soft costs—further enhancing project feasibility.

5. Expanding Global Footprint and Market Diversification

Emerging regions such as Asia-Pacific, Latin America, the Middle East, and Africa are becoming new centers of growth. Cervicorn’s analysis indicates these markets are witnessing significant acceleration, driven by rising solar capacity additions, favorable climates, and infrastructure development. Established markets like North America and Europe remain dominant but are now being complemented by rapid adoption across new geographies.

Market Drivers

The solar tracker market’s momentum is reinforced by several interconnected growth factors:

-

Utility-Scale Solar Expansion: The rising deployment of large-scale solar farms is increasing the demand for tracker-equipped sites that maximize yield and grid efficiency.

-

Declining Module and BOS Costs: Continuous reductions in PV module prices make the incremental cost of trackers more acceptable, with yield gains often exceeding 20%.

-

Government Incentives and Policies: National and regional renewable mandates, coupled with attractive tax credits and local content rules, are boosting adoption globally.

-

Technological Improvements: Modern trackers offer greater mechanical durability, advanced control systems, lower maintenance requirements, and extended warranties, improving reliability and ROI.

-

Land Efficiency and Yield Optimization: In land-constrained or high-cost areas, trackers provide a superior output-per-acre ratio, enhancing financial viability and project returns.

The Cervicorn Consulting report quantifies the combined effect of these drivers, projecting market growth from USD 10.67 billion (2024) to USD 42.43 billion (2034), achieving a 25.07% CAGR through the forecast period.

Impact of Trends and Drivers

The convergence of these dynamics influences market structure, technology adoption, and regional growth patterns:

-

By Application (Utility vs. Non-Utility): Trackers are most prevalent in utility-scale installations, where yield gains significantly enhance project economics. Smaller commercial and residential projects still lean toward fixed-tilt systems due to lower upfront costs and simpler installation.

-

By Type (Single-Axis vs. Dual-Axis): Single-axis trackers maintain dominance owing to cost advantages and simpler maintenance, while dual-axis trackers are gaining favor for projects that prioritize maximum generation efficiency.

-

By Region: Mature markets like North America and Europe continue to lead adoption due to advanced grid infrastructure and policy incentives. However, rapid capacity expansion in Asia-Pacific, Latin America, and the Middle East is propelling regional diversification and global demand stability.

-

System Integration and Digitalization: As solar plants increasingly combine PV, energy storage, and smart control systems, integrated tracker solutions are becoming a key value differentiator. Manufacturers offering data-driven performance optimization are positioned for stronger growth.

Challenges & Opportunities

Challenges

-

High initial investment and complex maintenance, especially in dual-axis systems.

-

Site-specific limitations (terrain, wind loads, or soil stability) that affect tracker deployment feasibility.

-

Market competition and pricing pressures amid increasing commoditization.

-

Continued preference for fixed-tilt systems in small or cost-sensitive installations.

Opportunities

-

Retrofitting and repowering older solar farms with advanced trackers for yield enhancement.

-

Integration of bifacial modules with trackers for improved energy capture and efficiency.

-

Untapped growth in emerging regions such as Africa, Southeast Asia, and Latin America.

-

Digital transformation enabling predictive maintenance, AI-driven optimization, and performance guarantees.

-

Hybrid solutions combining PV + storage + tracker systems that offer higher grid stability and project bankability.

Future Outlook

The global solar tracker market is entering a phase of accelerated expansion, characterized by technological maturity, cost competitiveness, and increasing policy alignment. By 2034, it is projected to reach USD 42.43 billion, growing at a CAGR of 25.07% from its 2024 valuation of USD 10.67 billion.

In the coming decade, widespread adoption across diverse regions, the integration of AI and automation, and the pairing of trackers with bifacial modules and energy storage will redefine project economics and performance. Manufacturers focusing on lightweight structures, modularity, and digital analytics are expected to gain a competitive edge as the industry scales toward the next generation of high-performance solar infrastructure.

👉 To Get a Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us