Market Overview

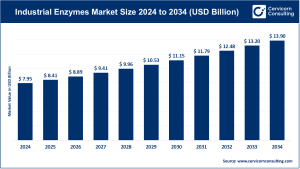

The global aluminum alloys market is witnessing consistent growth, underpinned by expanding industrial usage and increasing emphasis on sustainability. Valued at USD 156.71 billion in 2025, the market is anticipated to climb to approximately USD 283.47 billion by 2035, progressing at a CAGR of 6.1%. This upward trajectory is largely fueled by rising consumption across major end-use sectors such as automotive, construction, packaging, machinery, and electronics. Aluminum alloys continue to gain preference over conventional materials owing to their lightweight characteristics, corrosion resistance, durability, and strong recyclability profile.

Key Market Trends Shaping the Aluminum Alloys Industry

1. Lightweighting & Electrification in Transportation

A dominant trend influencing the industry is the accelerating shift toward lightweight materials, particularly within automotive and aerospace applications. Aluminum alloys are essential for reducing vehicle mass, enhancing fuel economy, and improving electric vehicle efficiency. Automakers are increasingly deploying high-strength alloys in structural parts, battery casings, and exterior panels. This transition aligns closely with tightening emission regulations and the rapid global adoption of electric vehicles.

2. Sustainability & Expansion of Recycled Alloys

Sustainability continues to define market evolution. Aluminum’s exceptional recyclability positions it at the center of circular economy strategies. A substantial portion of aluminum ever produced remains in circulation, highlighting its extended lifecycle benefits. High recycling rates—especially in beverage can applications—have stimulated investments in secondary aluminum production, which delivers considerable energy savings relative to primary manufacturing.

Get a Free Sample: https://www.cervicornconsulting.com/sample/2902

3. Increasing Demand for Low-Carbon Aluminum

Environmental mandates and corporate decarbonization objectives are driving demand for low-carbon aluminum alloys. Industries are progressively favoring materials that offer reduced carbon footprints. This trend is encouraging advancements in cleaner smelting processes, greater renewable energy integration, and certification frameworks for low-emission aluminum products.

4. Production Capacity Growth in Emerging Regions

Emerging markets, particularly in Asia and the Middle East, are reinforcing their positions as key aluminum producers. Competitive energy access and expanding industrial infrastructure have supported large-scale capacity enhancements. This geographic shift is reshaping global supply structures and strengthening export competitiveness.

Market Drivers Fueling Growth

Strong Demand from Automotive & Transportation

The automotive industry remains the leading consumer of aluminum alloys, accounting for approximately 30–31% of total demand. Ongoing lightweighting initiatives and electric vehicle expansion continue to elevate alloy consumption. Applications increasingly span chassis systems, powertrain components, and battery structures.

Rapid Urbanization & Infrastructure Development

Urban growth and infrastructure investment are significant market catalysts. Aluminum alloys are widely utilized in modern construction, including façades, windows, roofing, curtain walls, and structural assemblies. Their durability, corrosion resistance, and design adaptability make them highly suitable for residential and commercial developments.

Growth in Packaging Applications

Packaging represents a major contributor to aluminum demand, comprising roughly 16% of global consumption. Aluminum alloy packaging solutions are gaining traction due to sustainability advantages, recyclability, and superior barrier performance. Beverage cans, food packaging, and flexible formats remain key demand drivers.

Government Policies & Industrial Strategies

Policy frameworks promoting domestic production, recycling targets, and sustainability standards are shaping market expansion. Trade regulations, tariffs, and incentives supporting low-carbon materials are encouraging investment in regional manufacturing capacity and recycled alloy technologies.

Impact of Trends & Drivers on Market Segments

Regional Market Dynamics

-

Asia Pacific leads the global market, representing approximately 58% of total demand, supported by rapid industrialization, automotive output, and infrastructure development.

-

North America prioritizes strengthening domestic supply chains, recycling efficiency, and sustainable alloy innovation.

-

Europe emphasizes low-carbon materials and sustainability-focused advancements amid stringent environmental regulations.

-

Middle East & Emerging Regions benefit from cost-effective production and expanding downstream processing capabilities.

Challenges & Opportunities

Challenges

-

Energy-Intensive Production: Aluminum manufacturing remains heavily energy-dependent, exposing producers to fluctuations in energy pricing.

-

Regulatory Pressures: Carbon reduction targets and environmental compliance requirements contribute to rising operational costs.

-

Supply Chain Volatility: Trade policy changes and raw material price variability impact market stability.

Opportunities

-

Low-Carbon & Green Aluminum: Development of sustainable alloy solutions presents strong competitive differentiation.

-

Electric Vehicle Expansion: EV growth continues to unlock new, high-value alloy applications.

-

Advanced Alloy Technologies: Innovations in high-strength, lightweight, and heat-resistant alloys are enabling broader industrial usage.

-

Recycling & Circular Economy: Expansion of secondary aluminum production offers both economic and sustainability advantages.

Future Outlook

The aluminum alloys market is poised for stable long-term growth, projected to reach USD 283.47 billion by 2035, advancing at a 6.1% CAGR. Future development will be driven by transportation electrification, sustainability initiatives, technological advancements, and increasing substitution of heavier materials. Demand for low-carbon and recycled aluminum alloys is expected to play a pivotal role in shaping competitive strategies and investment decisions across the industry.

To Get Detailed Overview, Contact Us: https://www.cervicornconsulting.com/contact-us