Generative Al in Automotive Market overview

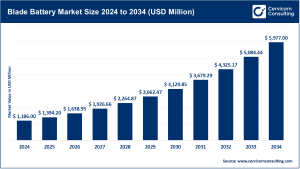

The Generative AI in Automotive market was valued at USD 482.23 million in 2024 and is forecasted to reach approximately USD 3,945.89 million by 2034, growing at a robust CAGR of 25.65% from 2025 to 2034. In terms of regional contribution, North America captured about 41% of market revenue in 2024, followed by Europe at 27%, while the U.S. market alone accounted for around USD 148.29 million. The market encompasses diverse segments, including vehicle types (passenger and commercial), technologies (machine learning, NLP, context-aware computing, computer vision, etc.), and applications such as vehicle design, manufacturing optimization, ADAS/autonomous driving, and logistics.

Key market trends

-

Generative AI in vehicle design & prototyping

Automakers are increasingly adopting generative AI to explore innovative design options, reduce component weight, minimize material use, and speed up prototyping. This trend enhances efficiency across R&D and supplier design ecosystems. -

Personalized in-vehicle assistants

AI-driven assistants are delivering conversational, context-aware support for infotainment, navigation, and vehicle controls. OEMs are embedding these systems as either value-added options or subscription-based features, reshaping the in-car experience. -

Advancements in ADAS & autonomous driving

Generative AI enables the creation of synthetic driving scenarios, especially rare or high-risk events, which strengthens the training of perception and decision-making systems without requiring massive real-world datasets. -

Connected mobility & smart-city integration

With cars increasingly interacting with urban infrastructure, generative AI supports real-time routing, fleet management, and predictive maintenance — essential for building efficient smart-city ecosystems. -

Shift toward subscription-based models

Automakers and suppliers are monetizing AI-driven features (premium navigation, predictive diagnostics, advanced driver assistance) through recurring subscription plans, moving away from traditional one-time hardware revenues.

Market drivers

-

Rising adoption of AI in the auto sector — Industry-wide AI integration for design, manufacturing, and self-driving systems has surged by over 40%, reflecting increased R&D investment.

-

Efficiency and cost optimization — Generative AI accelerates prototype development, cutting timelines by up to 25%, while logistics and supply-chain applications reduce costs by as much as 15%.

-

Safety and regulatory compliance — Enhanced safety features powered by AI contribute to roughly 20% improvements in accident prevention, aligning with regulatory mandates for safer and more sustainable vehicles.

-

Growing demand from commercial fleets — Predictive maintenance and optimized fleet management solutions are in high demand, as they directly improve uptime and profitability in logistics and transportation.

Impact of trends & drivers

-

Design & R&D acceleration — Early adopters of generative design benefit from shorter product development cycles and reduced material expenses, particularly in passenger vehicles.

-

Fleet & logistics optimization — Commercial operators see tangible returns through fuel savings and reduced downtime, making adoption highly attractive in last-mile delivery and large-scale logistics.

-

ADAS & autonomous growth — The use of synthetic data strengthens autonomous driving frameworks, with adoption advancing fastest in regions like North America and Europe where regulatory frameworks support testing.

-

Regional landscape — North America leads due to strong OEM and tech presence, Europe benefits from emission and safety-driven regulations, while Asia-Pacific is the fastest-growing region driven by EV adoption, scale in manufacturing, and smart-city programs.

Challenges & opportunities

Challenges

-

High capital requirements for AI infrastructure and integration.

-

Privacy and data security risks due to extensive data collection.

-

Diverse regulatory standards that complicate safety certification.

Opportunities

-

Lightweight vehicle design that supports sustainability goals.

-

Recurring revenues via subscription-based AI features.

-

Expansion into fleet management and smart-city services beyond vehicle sales.

Future outlook

The Generative AI in Automotive market is poised for rapid growth, expanding from USD 482.23 million in 2024 to ~USD 3,945.89 million by 2034, at a CAGR of 25.65%. The decade ahead will be shaped by breakthroughs in generative modeling, the rise of connected EV fleets, and new revenue models based on AI-driven services. Key developments to watch include cloud-to-edge OEM–tech partnerships, synthetic data for safer autonomy, and regulatory harmonization to accelerate deployment.

Executive takeaways

-

The market is at an early growth stage with high acceleration potential.

-

North America holds the largest share, while Asia-Pacific is set to outpace others in growth.

-

Short-term opportunities lie in fleet optimization, design cost savings, and subscription-based features, while long-term success hinges on addressing privacy, certification, and cost barriers.

👉 For deeper insights, visit Cervicorn Consulting’s Generative AI in Automotive Market report.